Enhancing the vehicle and ownership experience over time

Beyond common goods and services, certain features and technologies that weren’t initially offered or added to a vehicle at time of purchase can be downloaded later through an in-vehicle marketplace. These can include ADAS features, comfort amenities, and even performance-focused treats like quicker acceleration and extra range for EVs. “This opens the door for manufacturers to let an owner easily enhance and better their vehicle over time,” says Robby DeGraff, Manager of Product and Consumer Insights at AutoPacific. “Maybe you didn’t think you’d need a hands-free highway driving assist when you first drove your vehicle off the lot…but now you suddenly do because you’re road-tripping a lot. A few minutes and taps on the center touchscreen, and you’ve just upgraded your vehicle without ever stepping foot in a dealership.”

Concerns and considerations to ensure seamless transactions

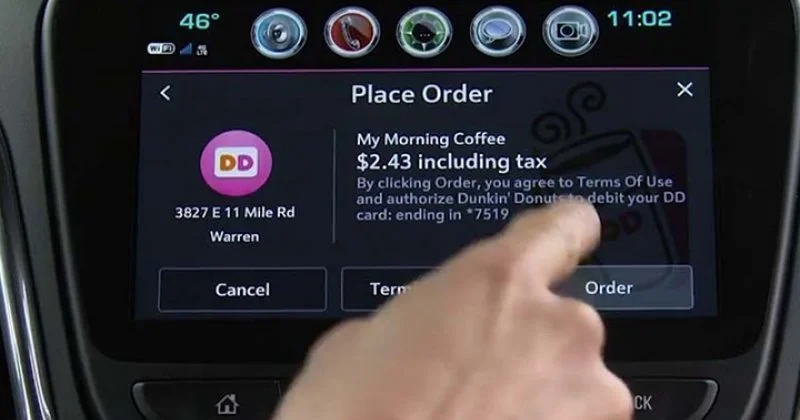

Earlier attempts at in-vehicle marketplaces were flawed by complicated on-screen steps, lagging connections and syncing of an owner’s payment methods, as well as a relatively small number of participating vendors. In order to ensure best practice for a consumer to purchase products, technologies, and vehicle upgrades directly from a center infotainment screen, the process must be as quick, easy, and straightforward as it would be to do so using a mobile device. Any interruption, glitches, or difficulty during an on-screen transaction would likely see the consumer immediately resorting to completing the transaction on their smartphone.

Furthermore, privacy may be a real concern for some consumers, even those open to having connected technology in their vehicle. 66% of all respondents, and 70% of those who want the ability to securely purchase products, technologies and upgrades from their vehicle’s center infotainment screen say they are concerned about their privacy due to use of various technologies. Transparency, a way to opt out of a transaction if desired, and of course security for all stored payment methods need to be guaranteed by the automaker.