by Robby DeGraff, Manager of Product and Consumer Insights

The ways auto insurance premiums are determined are evolving quickly. Even consumers with driving records clear of accidents and citations may be shocked as their policy rates rise significantly this year. As recent news reports have brought to the public eye, many automakers are partaking in a revenue-generating practice that’s escalating concerns about privacy: the monitoring and sharing of one’s driving behavior with their customers’ insurance companies, in some cases without the customer opting in. Aggressive acceleration, panic braking, and turbulent steering are all actions for which data can be recorded and shipped off to insurance companies to decide on a consequence. But what if this practice could be executed to benefit, not penalize the consumer?

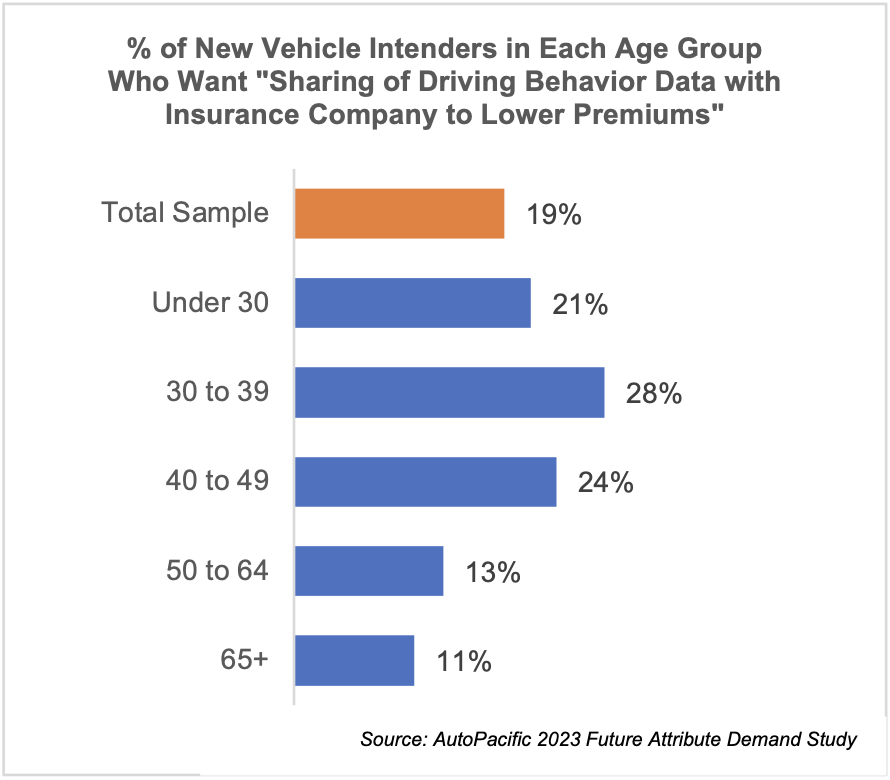

The Potential for Lowering Insurance Premiums Has Appeal

AutoPacific’s Future Attribute Demand Study found that 19% of consumers who plan to acquire a new vehicle within the next three years are interested in having a feature that shares driving behavior data with their insurance company to lower their premiums. Interestingly, and perhaps the result of dramatically rising auto insurance rates nationwide, demand for this feature grew +6% pts compared to last year’s study. I think the key part of this feature is lowering premiums; consumers want the benefit, but not the penalty.

Younger consumers, especially those ages 30-39, are the most interested in allowing their vehicle to keep tabs on their driving behavior in a hopeful bid to lower their insurance rates (28%), even despite being more concerned than other generations about their privacy due to in-vehicle technology use, Conversely, just 12% of consumers age 50 and older showed interest in this feature. Demand is also much higher among households with children than those without (+12% pts), perhaps reflecting many families’ need to explore ways to free up more funds for this expensive life stage.

Sharing of Driving Data Could Result in Higher Premiums for Many, Hurt Consumer Trust

Despite the potential for data sharing to reduce premiums, it could raise premiums for many drivers since their vehicles can record and share data about driving habits that insurance companies view as negative. Combined with reports that some automakers are selling that data to insurance companies without their customers opting in, this practice has a high probability of eroding consumer trust in many cases. Automakers can and should offer much more transparency about how their data is being used and ensure that consumers are not automatically and unknowingly participating by default. I beleive trust is a critical part of the relationship between the automaker and consumer and automakers must consider the long-term consequences of sharing their customers’ personal data.